San Francisco Bay Area Residential Real Estate Trends: March 2026 Market Report

Spring has brought new life to the Bay Area property market. After a muted start to the year, buyers have returned with vigor. Multiple-offer situations have become common again, and some single‑family homes are fetching 25–50 % above list price in desirable neighborhoods. Condominiums, which spent much of last year languishing on the market, are also seeing increased foot traffic. Inventory is still tight in absolute terms, but it has improved compared with early winter. As a result, the available supply is being snapped up quickly. In this report, you’ll find a concise snapshot of last month’s sales data, insight into what’s driving the momentum, individual county highlights, a macro overview, and a discussion of the economic and policy factors shaping our housing landscape.

Local Market Insight

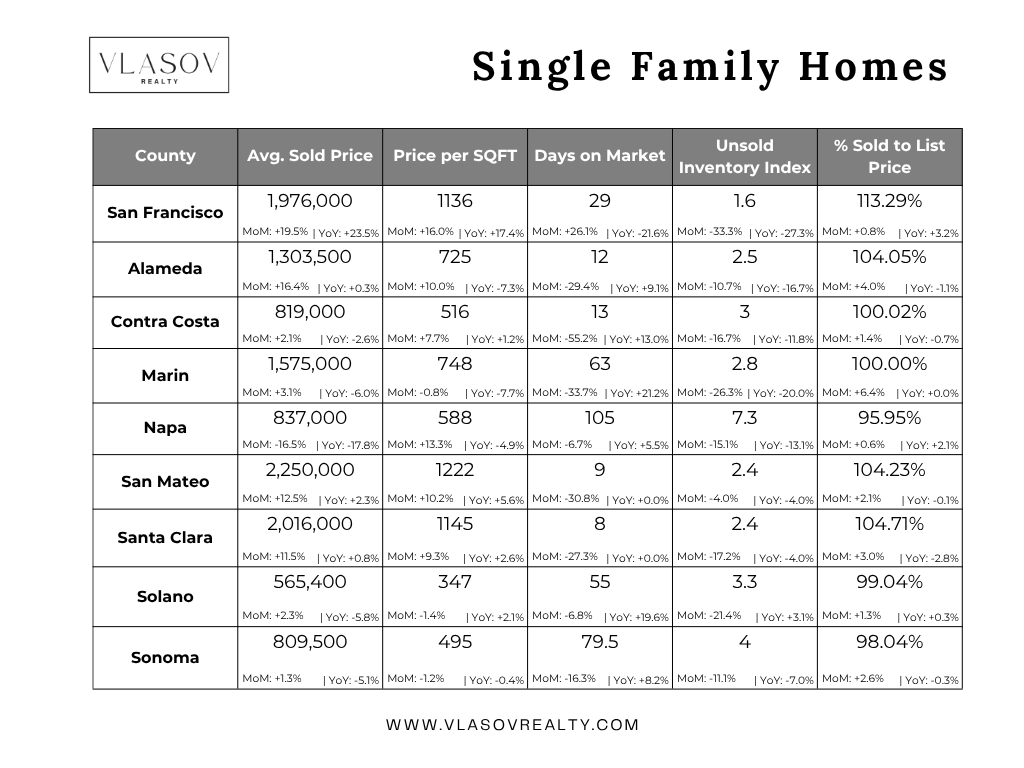

February’s sales figures confirm what boots‑on‑the‑ground observers have felt for weeks: the market momentum is building across nearly every Bay Area county. Median prices rose month‑over‑month in all nine counties, and year‑over‑year comparisons were positive in most areas. Sales volumes also surged, with monthly increases ranging from 30% to over 90%, depending on the county. These numbers indicate that buyers who were previously waiting on the sidelines, hoping for deeper price cuts or lower interest rates, have decided that this spring presents a window of opportunity.

At the county level, San Francisco delivered a standout performance. The city’s median single‑family home price jumped to about $1.976 million, up 19.5 % from January and nearly 4.3 % higher than February 2025. More strikingly, home sales in the city surged 93.3% month‑to‑month, reflecting a spike in buyer activity despite prices that remain among the highest in the nation. San Mateo remains the most expensive county, with a median price around $2.25 million and healthy double‑digit growth both month‑to‑month and year‑over‑year. Santa Clara followed closely, with a median price near $2.016 million and an astonishing 70.1% increase in monthly sales. Even more affordable areas such as Solano and Contra Costa saw median prices climb, while sales volumes increased by roughly 31–41%. In short, the February numbers suggest the Bay Area’s housing engine is running on all cylinders.

What’s Driving the Market

-

Low but improving inventory. After two years of historically low listings, many homeowners who locked in sub‑3 % mortgages are still reluctant to sell. However, some inventory has come back as people relocate for work or personal reasons. Slightly more supply plus pent‑up buyer demand leads to bidding wars.

-

Easing mortgage rates. While rates remain well above their 2021 lows, the average 30‑year fixed rate hovered around 6.11 % in early March—down from 6.65 % a year ago. Forecasts from Fannie Mae and other analysts expect rates to drift toward the mid‑5 % range by late 2026, giving buyers confidence that their borrowing costs may decline further.

-

Booming tech and AI sector. Bay Area job growth, particularly in artificial intelligence and cloud computing, has fueled wage gains and equity windfalls for many professionals. Companies like OpenAI, Anthropic, and the major cloud providers are expanding local hiring. Fresh wealth and stock‑based compensation are translating into higher housing budgets.

-

Return of commuter demand. Hybrid‑work arrangements are drawing some employees back to the office several days a week, reigniting demand for homes with reasonable commute times to downtowns or major employment hubs. This is particularly evident in central counties like San Mateo and Santa Clara, where buyers prioritize access to freeways and public transit.

County Highlights

San Francisco: High-priced homes are again attracting multiple offers. especially modern condominium buildings near transit, though price appreciation remains stronger for single‑family homes. The surge in sales suggests renewed confidence in urban living.

East Bay (Alameda and Contra Costa): These counties continue to benefit from spillover demand and calmer market activities. Good schools and reasonable commute options keep families interested. Alameda’s median price climbed above $1.3 million, while sales rose more than one‑third over January.

North Bay (Marin, Napa, Sonoma): Demand for lifestyle properties remains steady. Marin posted a median price above $1.5 million and strong year‑over‑year growth. Napa’s prices dipped slightly from a year ago, but sales volumes jumped by more than 18%. Sonoma’s market was flatter year‑over‑year but remains stable and attractive to second‑home buyers.

Peninsula and Silicon Valley (San Mateo & Santa Clara): These counties are the epicenter of tech hiring and thus continue to command the highest prices. San Mateo’s median price of $2.25 million leads the region, while Santa Clara isn’t far behind. Both counties saw strong double‑digit increases in sales.

Solano County: As the most affordable county in the region, Solano is drawing first‑time buyers priced out of other areas. Prices remain under $600k, but monthly sales spiked by more than 40%.

Macro Market Overview

United States: Nationally, the median existing‑home price in February was about $398,000, up from $396,800 a year earlier. Single‑family home sales remain constrained by limited inventory, and the average 30‑year mortgage rate around 6.05 % in February was down from 6.84 % a year ago. The South and West regions of the country posted the largest year‑over‑year price gains. However, the national market remains balanced overall, with moderate price appreciation and flat sales compared with last year.

California: The state’s median home price was $830,370 in February, rising 0.9 % from January and slightly higher than a year earlier. Statewide sales increased month-over-month but were down 0.3% from February 2025. The San Francisco Bay Area outperformed the rest of the state, with a 2.8 % year‑over‑year price increase and a 4 % year‑over‑year sales gain. This divergence highlights the region’s resilience even as other parts of California experience softer demand.

Economic Factors

Inflation remains under control: the Consumer Price Index (CPI) rose 2.4 % year‑over‑year in February, while the “core” CPI (excluding food and energy) climbed 2.5 %. Moderating inflation has allowed the Federal Reserve to maintain a cautious stance; futures markets expect one or two rate cuts later this year. The 10‑year Treasury yield, a benchmark for mortgage rates, averaged 4.13 % in February, down from 4.21 % in January, suggesting bond investors expect slower growth.

The U.S. dollar index (DXY) has hovered above 100 amid safe‑haven demand driven by Middle East tensions. Analysts anticipate the dollar will trade in the 98–102 range in the coming months, with a weakening bias if the Federal Reserve cuts rates. Stock markets have been resilient despite geopolitical volatility; the S&P 500 ended flat in early March, with gains in energy, tech, and defense stocks offsetting losses elsewhere. Healthy equity markets and strong employment support housing demand, particularly in tech‑heavy regions like the Bay Area.

Mortgage Rates

For most buyers, mortgage rates are the deciding factor. As of March 12, Freddie Mac reported that the 30‑year fixed‑rate mortgage averaged 6.11 % and the 15‑year fixed averaged 5.50 %, both up slightly from the prior week but down from 6.65 % and 5.95 %, respectively, a year earlier. Although rates remain elevated compared with 2021, they are below the peak reached last fall. Market expectations suggest that rates could fall into the mid‑5 % range by the end of 2026, according to forecasts from Fannie Mae and the National Association of REALTORS®.

Several factors influence the rate outlook:

-

Federal Reserve policy. The Fed has signaled it may cut rates later this year if inflation stays near target, which would lower mortgage costs. However, it remains data‑dependent.

-

Economic growth. Faster growth typically pushes rates higher; slower growth or recessionary fears exert downward pressure.

-

Global demand for safe‑haven assets. International events can spur demand for U.S. Treasury bonds, driving yields down and, along with them, mortgage rates. Recent geopolitical tensions have kept yields higher than they might otherwise be.

-

Lender spreads. Banks adjust rates based on risk premiums, supply and demand in the secondary market, and regulatory requirements.

Borrowers who can qualify today might choose to lock in a rate before expected cuts to ensure affordability. Others may take short‑term adjustable-rate mortgages in anticipation of refinancing in 2026, when rates may be lower. Speak with a mortgage professional to evaluate options.

Housing Policy & Development

Recent legislation and policy changes are reshaping how and where homes can be built. Here are some of the key initiatives for 2026:

-

Transit‑oriented development: SB 79 allows housing projects near transit stations to override local zoning ordinances. Transit agencies can set new standards for density and height, accelerating mixed‑use developments.

-

Accessory dwelling units (ADUs): SB 9 invalidates local ADU ordinances that haven’t been submitted to the state for review; SB 543 clarifies that only interior livable space counts toward ADU size limits and exempts ADUs under 500 sq ft from school impact fees. AB 462 streamlines coastal permit reviews for ADUs and allows separate occupancy certificates.

-

Junior ADUs: AB 1154 removes owner‑occupancy requirements for junior ADUs and prohibits them from being used as short‑term rentals.

-

Permit streamlining: AB 920 requires large cities and counties to implement online permitting portals, while AB 1308 mandates that building departments inspect small projects within ten days. AB 253 allows private plan‑checkers to expedite permitting if local agencies take longer than 30 days.

-

Historic protections: AB 1061 refines SB 9 by shifting historic‑protection exemptions from broad districts to specific structures, allowing cities to adopt objective standards.

These measures aim to ease the state’s housing shortage by encouraging denser development around transit, simplifying the permitting process, and protecting homeowners who add second units. Bay Area cities with ambitious transit‑oriented plans, such as San Francisco’s downtown rail extension and San Jose’s Diridon Station redevelopment, are likely to benefit the most.

Local Insight

Open houses are busy again, and motivated buyers are making strong offers early in the listing period to avoid bidding wars. Sellers who price strategically are rewarded with multiple offers, while those who overprice still sit. Condominiums that were tough sells last year are moving thanks to improved mortgage affordability and renewed appetite for urban amenities. Investors are also back in the game, recognizing the long‑term growth potential of the Bay Area’s tech and biotech economy.

While some might worry that we’re headed toward another unsustainable run‑up, today’s environment differs from the last housing bubble. Lending standards remain stringent, buyers are better capitalized, and the tech sector’s growth is real. That said, I expect price appreciation to moderate later in the year as more inventory comes online and buyers become more rate‑sensitive. For now, the message to prospective buyers is clear: if you find a property that meets your needs and budget, act decisively. For sellers, this spring presents a prime window to list while demand is still outstripping supply. If you have questions about your neighborhood or need guidance on pricing, feel free to reach out. I’m happy to share more specific market intelligence.

Categories

Recent Posts

Stay In The Know - Subscribe To Market Updates

LET'S GET IN TOUCH