San Francisco Bay Area Residential Real Estate Trends: January 2026 Market Report

January 2026 opened the Bay Area housing market with a theme of transition and moderation. After several years of pandemic-era volatility, key indicators suggest the region is shifting toward a more balanced environment between buyers and sellers. Mortgage rates have eased from last year’s highs, inventory is no longer frozen at historic lows, and seasonal “reset” behavior is shaping buyer expectations. While prices remain elevated, buyers are re-engaging with purpose as the market adjusts to steadier conditions.

Local Market Insight

Across Bay Area counties, median prices remain significantly higher than pre-pandemic levels, though the pace of appreciation has cooled compared to the red-hot years. January data reflects normal seasonal behavior lower transaction volume than summer, longer time on market, and more pragmatic negotiation. Inventory has ticked higher, providing buyers with slightly more choice, and sellers are relearning the importance of accurate pricing rather than relying on peak-era momentum.

The Bay Area still outperforms national figures on pricing and demand intensity, but the drivers have shifted. Strong homes in desirable neighborhoods move quickly, while overpriced listings sit. This month is more about fundamentals, with a noticeable trend of buyers returning after the holidays, pre-approved, and with realistic goals.

What’s Driving the Market

1. Seasonal Shifts in Demand

January always restarts momentum. Buyers who paused in Q4 re-enter the market with fresh timelines, school planning, relocation needs, and financial resets.

2. Mortgage Rate Stabilization

Rates have come off their late-2025 peaks. They are not “cheap” by decade standards, but they have become more predictable, and predictability encourages action.

3. Inventory Improvement

Listings began hitting earlier this season than in the past two years, easing extreme scarcity. It’s not a surplus, but it’s enough to change negotiation dynamics.

4. Local Economic Stability

The Bay Area’s employment base in AI technology, biotech, digital media, and knowledge-based sectors remains resilient. Income stability supports buyer confidence, even when affordability is tight.

Together, these factors are creating a market with balance rather than pressure, a positive sign for long-term health.

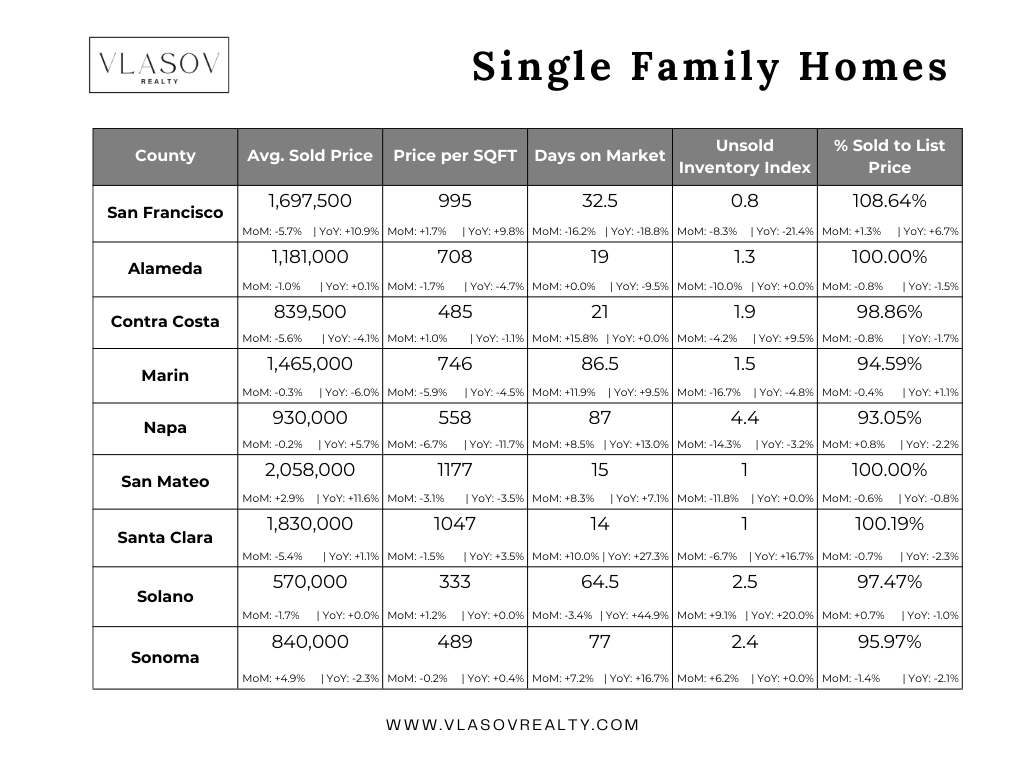

County Highlights

San Francisco

SF feels like it’s waking up after a slower Q4. The big shift this month is buyer decisiveness: serious tours increased, especially in family neighborhoods and renovated inventory. The driver here is a clearer rate environment and renewed confidence from dual-income tech households who sat on the sidelines during rate volatility. Condos are showing early momentum in the 1.1–1.6m range, where sellers adjusted pricing during Q4 and buyers are now stepping in. The luxury segment remains steady, with fewer listings but purposeful buyers.

Marin

Marin saw a jump in qualified buyer inquiries as soon as the new year hit. This month’s main driver is lifestyle relocation buyers who already made the “do we move to Marin?” decision in 2025 and are now executing on it. Time on market shortened for well-presented listings in Mill Valley and Corte Madera, while larger estate properties are getting more tours but still face drawn-out negotiations due to renovation uncertainty and holding costs. Inventory remains limited, and that constraint is keeping sellers confident on pricing going into spring.

San Mateo

San Mateo County is showing one of the clearest “market is waking up” signals. Buyer activity picked up meaningfully in the mid-range ($1.8–$2.7m) SFH segment, driven by rate stabilization and school-year planning. A notable shift this month: more move-up buyers listing their homes. It loosens inventory by increasing net new listings rather than just absorbing supply. Days on market compressed for remodeled stock, while original-condition homes are sitting longer as buyers factor in renovation timelines and contractor availability.

Santa Clara

Santa Clara is back on tech confidence. The difference from last month is that touring volume and pre-approvals jumped right after the New Year rather than late spring. Driven by rates stabilized, and job cuts slowed, so qualified tech buyers are stepping back in instead of waiting for theoretical rate cuts. Cupertino, Sunnyvale, and West San Jose saw competitive bidding reappear at the edges, not 2021 intensity, but enough to establish clear pricing floors. Condos are also moving faster than last quarter, driven by improved relative value compared to SFHs.

Alameda

Alameda County’s shift this month is inventory clarity. December had uneven supply; January brought a cleaner spread of new listings, giving buyers actual choice and letting comps reset. Touring volume in the Oakland/Berkeley hills and the 1–1.5m interior markets ticked up. The main driver here is value alignment: buyers are comparing East Bay options against Peninsula/SF and realizing that floor plans, yards, and neighborhoods better align with family needs at the same price. The immediate result this month: more serious offers, fewer “wait and see” buyers, and more sellers accepting small concessions to wrap deals before spring.

Contra Costa

In Contra Costa, January’s momentum is coming from sequenced buyer planning. Families relocating from SF and West Berkeley are touring with the intention to write by March, not “sometime this year.” This creates a pipeline effect: January is heavy touring and disclosure review, February/March becomes the transaction window. Walnut Creek, Lafayette, and Danville are seeing strong open house traffic for remodeled inventory, while older ranch product draws interest but slower conversions. Families want to secure housing before late spring so they can enroll without stress.

Sonoma

Sonoma saw an interesting January: luxury and second-home touring improved, even as transaction volume remained winter-soft. cCarity + lifestyle calculation: buyers are running numbers for weekend homes again because they know roughly what their mortgage payment will be, unlike the volatility of 2022–2023. Healdsburg and Sonoma proper are getting the most attention; Russian River areas still face insurance and underwriting hesitation. Expect more conversions in spring as the weather and inventory improve.

Napa

Napa’s activity this month is coming from long-term second-home buyers and investor-users. Touring increased for properties with either vineyard adjacency or strong rental potential. The shift from last month is that buyers are no longer waiting for price breaks; they’re negotiating terms, credits, and repairs. Sellers who overpriced in late 2025 have adjusted, making January feel more aligned and less aspirational. The main driver is strategic wealth deployment into hard assets with lifestyle upside.

Solano

Solano’s January story is early-year affordability pressure releasing just enough to pull new buyers back in. This month saw an uptick in FHA and conventional pre-approvals in the 450k–650k range, and that is translating into more showings and fewer stale listings. The driver is simple and tactical: rates relaxed, payments penciled, and inventory exists. Unlike last year, first-time buyers are writing offers earlier in the year instead of waiting until May–June. Vacaville and Fairfield are showing the most energy, particularly for updated homes with clean disclosures.

Macro Market Overview

On the national level, housing activity in late 2025 and early 2026 shows stability with modest growth, but not the sharp acceleration seen earlier in the decade. The U.S. median existing home price sits near $405,000, slightly above last year’s levels, indicating stable prices and modest year-over-year growth. Market momentum remains subdued, with sales volume gradually increasing alongside rising inventory, which has pushed the median days on market to around 60, longer than the ultra-tight conditions of recent years. This mix of steady prices, growing inventory, and slower movement suggests a balanced rather than overheated national market.

In California, instead of price growth, the statewide median price in late 2025 reflected a YoY decline of roughly 1%–2%, marking a mild cooling rather than a structural downturn. Importantly, this cooling is paired with a longer selling cycle, as days on market in California have increased year-over-year into the low-50-day range, indicating slower absorption even as buyer activity improves.

Economic Factors

Heading into 2026, the broader U.S. economy is operating in a slower but stable gear. Inflation has cooled from its pandemic-era peak. Headline CPI is roughly 2.7% year-over-year, and core CPI is around 2.6%, much closer to the Fed’s 2% target. This easing has helped stabilize input costs for businesses and reduced volatility in consumer spending. The stock market reflected this shift through late 2025, with major indices trending higher on expectations of sustained disinflation and a soft-landing scenario rather than a recession. The business cycle today is defined by controlled normalization, companies are still hiring, corporate earnings are steadier, and consumers are spending with more discipline.

The labor market remains a key anchor in this environment. Unemployment is low by historical standards, job openings have fallen from extreme highs, and wage growth has cooled to roughly match inflation, meaning real purchasing power is no longer eroding month after month. Hiring has slowed from the breakneck pace of 2021–2023, but not collapsed, indicating a softening without deterioration. From a housing perspective, this matters because confidence in income stability is what ultimately drives household formation, relocations, and long-term planning.

Housing Policy and Development

On the policy side, California continues to push zoning and permitting reforms to increase housing density, particularly around transit corridors. Accessory Dwelling Units (ADUs) remain a major focus, with municipalities refining permitting processes to accelerate production.

In the Bay Area, multiple multi-family and mixed-use projects are advancing through review and entitlement processes, reflecting long-term demand. San Francisco has been adjusting elements of its planning and zoning framework to encourage residential conversions and new development, particularly in the urban core.

Statewide, updated Regional Housing Needs Assessment (RHNA) targets continue to pressure cities to plan for more units across income levels, though actual production is still constrained by labor, financing, and community opposition.

Mortgage Rates

Mortgage rates continued to ease into early 2026, with the average 30-year fixed slipping toward the high-5% to ~6.0% range, marking the first time in several years that borrowers have seen rates below 6%. For comparison, the same product in early 2025 was roughly around 7%, so the year-over-year drop is meaningful. The main forces behind the decline: inflation has fallen back toward the mid-2% range, recession risk has faded, and economic expectations are no longer forcing lenders to price in heavy inflation premiums. Bond markets have also shifted; the 10-year Treasury yield has come down from its peak, and because mortgage pricing follows the 10-year more closely than the Fed rate, lenders have room to price loans more competitively.

Whether these levels hold depends on the same variables that pushed them down. If inflation remains in the low-2% range and economic growth stays steady rather than overheating, there is a reasonable path for mortgage rates to hover around the 6% mark through much of 2026. If inflation reaccelerates or bond yields rise, rates could drift back up. If the economy softens and the bond market rallies further, rates could trend deeper into the mid-5% range. For now, the market is in a “wait-and-confirm” posture: rates are lower than last year, volatility has eased, and borrowers are finally able to plan rather than react, a shift that directly supports renewed buyer activity in the Bay Area and beyond.

Local Sentiment

From the perspective of real estate professionals, sentiment feels cautiously optimistic. Sellers who price realistically are seeing healthy showing activity and offers. Buyers are focused on condition, price fairness, neighborhood, and lifestyle fit rather than sprinting to beat rate hikes. Agents report negotiations based on data and logic rather than urgency and fear of missing out.

It feels like a “professional market” again, where representation, pricing strategy, staging, inspection preparation, and negotiation quality matter.

If you’re planning a move in 2026, buying, selling, investing, or repositioning, now is the time to get informed. Inventory is improving, rates are stabilizing, and the market is rewarding preparation and strategy. If you want a data-driven breakdown for your specific city or price point, reach out, and I’ll walk you through it with clarity, not pressure.

Categories

Recent Posts

Stay In The Know - Subscribe To Market Updates

LET'S GET IN TOUCH